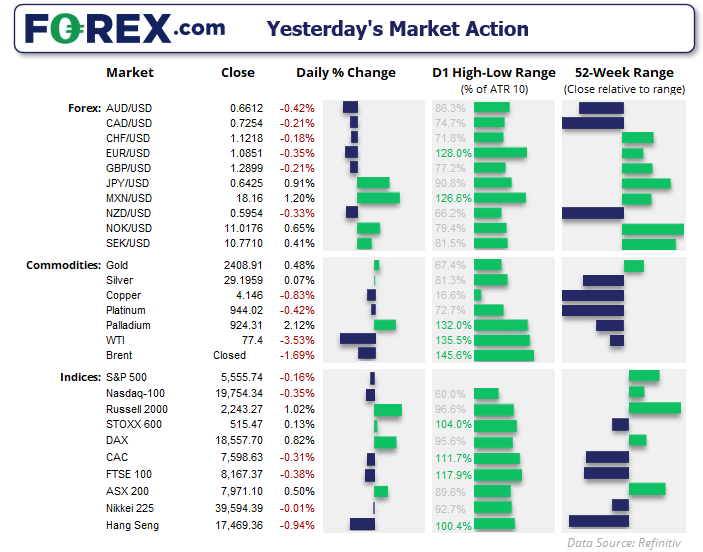

The Japanese yen was the strongest forex major on Tuesday ahead of next week’s BOJ meeting, Japan’s senior ruling party official Motegi called for the central bank to more clearly indicate its path to normalise policy (hike rates). A government spokesman also called for broad-based wage hikes to send the yen broadly higher against all FX majors. It remains an outside chance that the BOJ will opt to hike at next week’s meeting, although speculation is once again building that the central bank could consider hiking rates sooner than later.

USD/JPY was lower for a second day and closed below 156 for the first time since early June. EUR/JPY fell over -1% for the third time in eight days, saw a clean break of the December trendline to a 5-week low. A move to 168 or the June low appears to be on the cards. GBP/JPY appears to be headed for 200, where the cross might be able to find some support around its January 2024 trendline. Antipodean currencies are buckling under the pressure as carry trades are unwound on the combination of weak China growth, lower commodity prices and the prospects of a marginally more hawkish BOJ. AUD/JPY has fallen nearly -6% from the July 11 high closed below 103 and appears poised to test the June low in today’s session.

AUD/USD continued to track copper prices lower for a seventh consecutive day, as markets deemed the China Communist Party’s (CCP) third Plenum a non-event and deemed Monday’s interest rate cuts inadequate to support the global growth they crave from the world’s second largest economy.

The USD posted minor gains to a 5-day high, sending EUR/USD to an 8-day low.

Spot gold prices snapped a 4-day losing streak in line with yesterday’s bias, after finding support at the June high. I took a closer look at gold futures market positioning in yesterday’s article to highlight a sentiment extreme for the bull camp. Whilst I see the potential for another leg lower for gold, the bias remains for a move towards 2420 at a minimum before momentum turns lower. Bulls could seek dips within Tuesday’s range for near-term longs.

Events in focus (AEDT):

Were it not for flash PMIs, today’s calendar would be very bare apart from the Bank of Canada’s meeting (BOC). With China being the main driver for AUD and NZD pairs, I doubt their PMIs will make much of a dent for AUD/USD which is tracking commodities lower. A hot set of PMIs from Japan could support the yen on further speculation that the time for BOJ action could be approaching. Whereas traders will be on the lookout for further weakness in US data to justify their dovish market positioning.

The BOC are expected to cut their cash rate by 25bp to 4.5% to mark their second cut this cycle, and at back-to-back meetings. But like their first cut, I doubt they will signal further cuts and retain their patient stance.

- 09:00 – AU flash PMIs

- 10:30 – JP flash PMIs

- 13:00 – NZ credit card spending

- 16:00 – DE consumer sentiment (GfK)

- 17:15 – FR flash PMIs

- 18:00 – EU flash PMIs

- 18:30 – UK flash PMIs

- 22:00 – ECB Lane speaks

- 23:45 – BOC interest rate decision (-25bp expected)

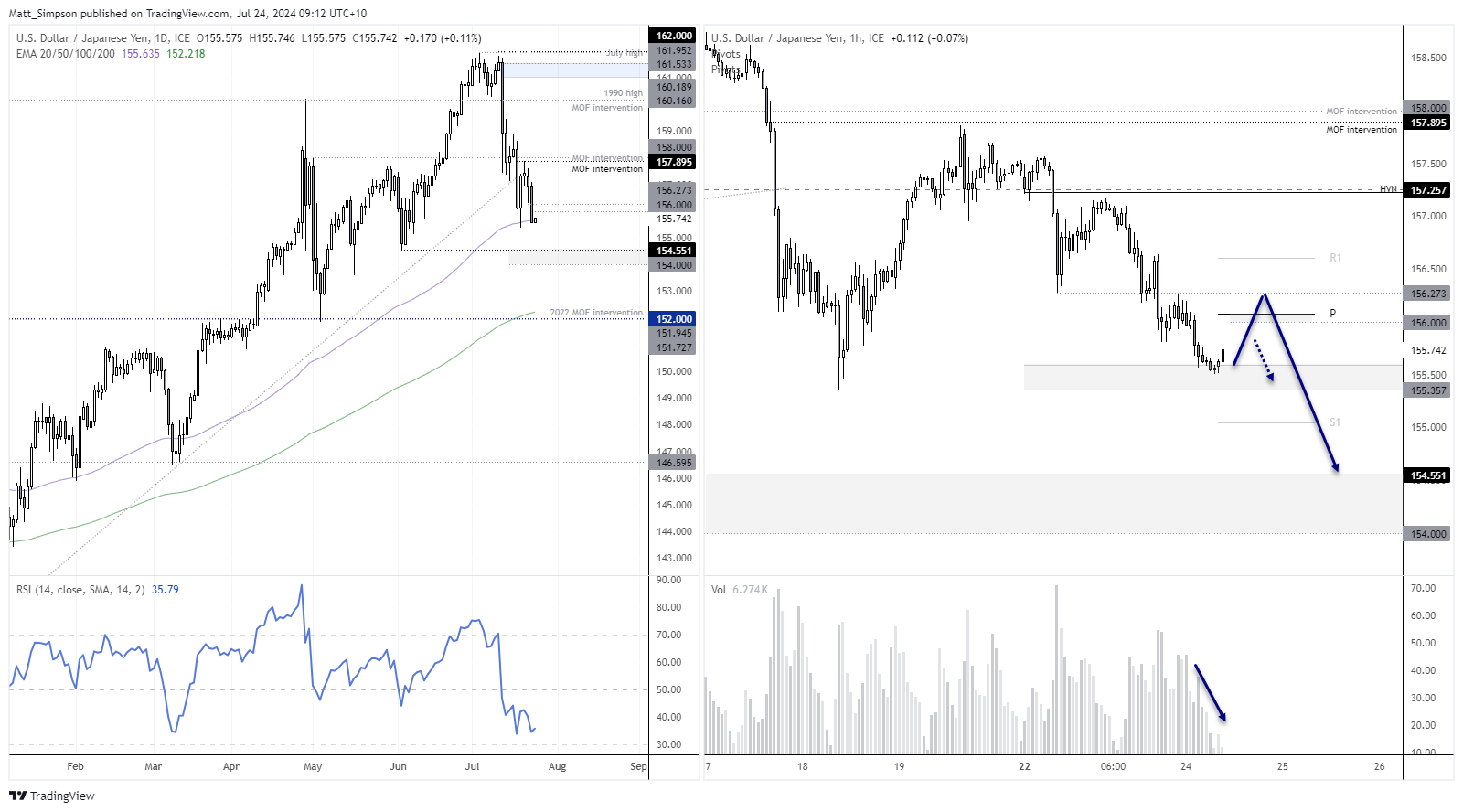

USD/JPY technical analysis:

Momentum has clearly sided with USD/JPY bears since the June high, and a retest of 154 seems more likely than not. However, the 100-day EMA is providing support and prices are holding above last week’s low, so perhaps there is room for a cheeky bounce first.

The 1-hour chart shows volumes were diminishing whilst prices fell in the US session, which suggests bears are losing steam. Support was also found near the weekly S1 pivot (155.59). Therefore, bears could seem to fade into strength today. Momentum is already trying to turn higher ahead of the Tokyo open, which brings 156 or the 156.27 low into focus for intraday bulls to target or bears to wait for evidence of a swing high.

View the full economic calendar

-- Written by Matt Simpson

Follow Matt on Twitter @cLeverEdge

Latest market news

Today 08:53 AM

Yesterday 11:26 PM

Yesterday 05:00 PM

Latest articles

Yesterday 11:26 PM

August 6, 2024 11:03 PM

August 5, 2024 11:06 PM

August 1, 2024 11:08 PM