US futures

Dow future 0.67% at 39,000

S&P futures 0.77% at 5416

Nasdaq futures 0.93% at 19390

In Europe

FTSE 0.99% at 8220

Dax 1% at 18574

- US CPI cools to 0% MoM in May from 0.3%

- Core inflation cooled to 3.4% YoY from 3.6%

- The Fed is not expected to cut rates

- Oracle rises after cloud deals announcement with Google & Open AI

Stocks rise as inflation eases, FOMC

U.S. stocks point to a strong open after US inflation cooled by more than expected and as investors look ahead to the FOMC rate decision later.

US CPI eased to 0% MoM in May, down from 0.3% in April and below the 0.1% forecast. On an annual basis, CPI remained unchanged at 3.4%. Core inflation, which strips out volatile items such as food and fuel, eased to 3.4% YoY, down from 3.6% and below estimates of 3.5%.

The cooler-than-forecast data has raised expectations that the Fed could cut rates sooner, pulling USD lower and boosting stocks.

Attention now turns to the FOMC rate announcement in a few hours. The Fed is expected to leave interest rates unchanged, so the main focus will be on the policy statement, updated projections, and dot plot, along with Federal Reserve chair Jerome Powell's press conference.

The policy statement is expected to confirm that the central bank needs more evidence of inflation cooling towards the 2% target before cutting rates.

However, the dot plot is likely to be revised lower. The Fed will struggle to justify three rate cuts this year, which were forecast in March. Given the hotter-than-expected inflation in the first quarter and the strength of the labour market, the dot plot will likely show two or even one rate cut in 2024.

Meanwhile, a slightly cautious-sounding Jay Powell could also push back rate-cut bets. While inflation appears to be on the right trajectory, it is still well above the 2% target.

Corporate news

Apple is holding steady at a record high after rising over 7% in trading yesterday following Apple’s unveiling of its AI strategy. After an initial tepid response to Apple's effort, the share price reversed higher on optimism that it will fuel an upgrade cycle.

Oracle is set to open 7% higher after the tech firm announced cloud deals with Google and OpenAI, which overshadowed a miss in fiscal Q4 results. Oracle posted EPS of $1.63 on revenue of $14.29 billion, below expectations of $1.65 on revenue of $14.55 billion.

Broadcom is expected to release earnings after the close. EPS is expected to rise to $10.85, up from $8.39 in the same period last year, and revenues of $12.06 billion, an increase of 38% as the company quietly penetrates the artificial intelligence landscape.

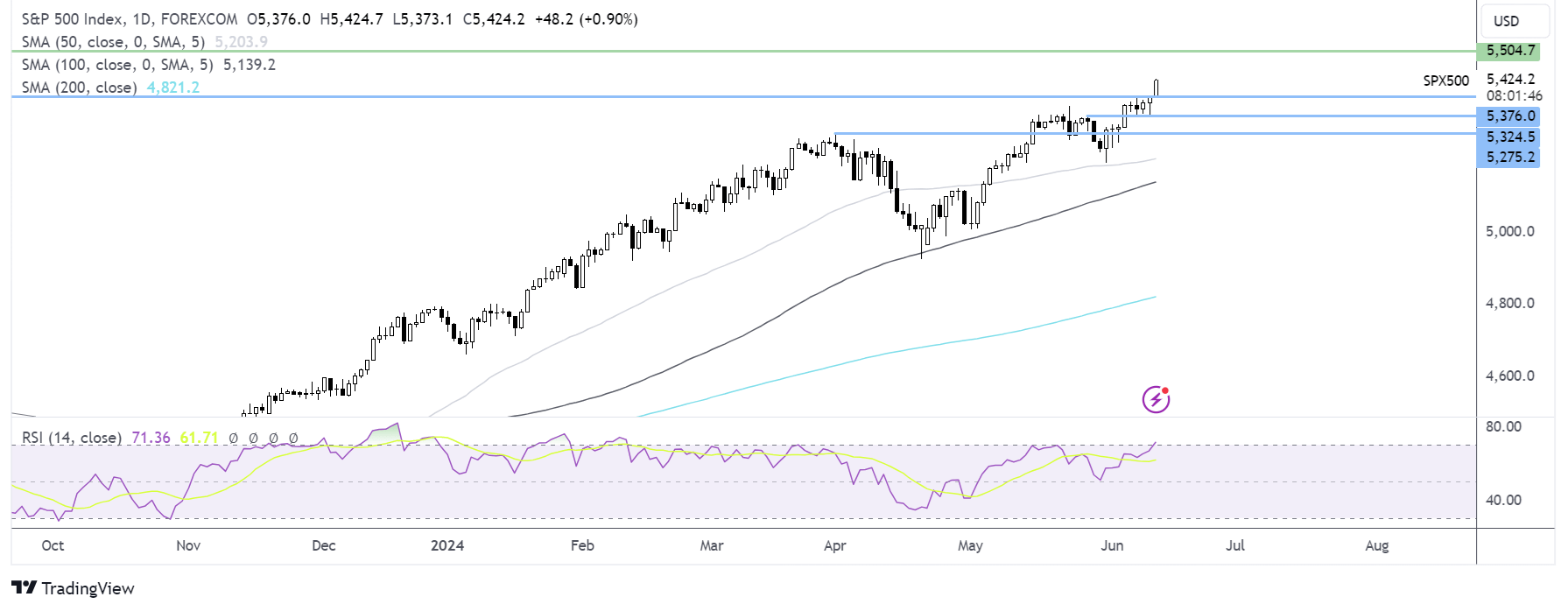

S&P 500 forecast – technical analysis.

The S&P500 has risen to fresh ATHs above 5400. Should buying momentum continue, 5500 will be the next logical target. The RSI has tipped into overbought territory, so buyers should be cautious. Support can be seen at 5376, last week’s high, ahead of 5330, the weekly low. Below here, 5277 comes into play.

FX markets – USD falls, EUR/USD rises

The USD is falling sharply after the cooler-than-forecast CPI data sees investors bring forward rate cut expectations.

EUR/USD is rising on a weak USD and after German inflation was upwardly revised to 2.8% YoY in May, up from 2.4% in April due to an acceleration of services inflation. Hotter inflation in the eurozone's largest economy raises questions over when the ECB will cut rates again after a 25 basis point cut last week. Meanwhile, ongoing political uncertainty in France, the eurozone's second-largest economy, could limit gains.

GBP/USD is rising on a weak USD despite signs that the UK's economic recovery has stalled. UK GDP slowed to 0 % MoM in April, down from 0.4% in March, as high interest rates put brakes on business and consumer growth. The data comes after the unemployment rate rose to a 2.5-year high, making a rate cut by the Bank of England at the August meeting more likely.

Oil rises on falling H2 inventory forecasts.

Oil prices are rising for a third straight day on expectations of lower global oil inventories in the second half of this year.

This week, the EIA, IEA, and OPEC released their monthly oil demand-supply outlook for the year. They pointed to a decline in global inventories, which could limit the downside in oil prices.

These views were supported by data yesterday showing that US crude oil inventories fell more than expected last week. EIA inventory data is due shortly.

The IEA downwardly revised its oil demand growth forecast to under 1 million barrels per day due to weaker consumption in developing countries. However, the IEA also sees demand growth topping out in 2029, which could result in a supply glut by 2030.

Yesterday, the EIA raised its 2024 world oil growth demand forecast to 1.1 million bpd while OPEC stuck with its forecast of 2.25 million bpd.

Latest market news

Today 12:00 PM

Today 08:53 AM

Yesterday 11:26 PM

Yesterday 05:00 PM

Latest articles

July 26, 2024 01:32 PM

July 25, 2024 01:17 PM

July 24, 2024 01:43 PM

July 23, 2024 01:38 PM